A Retirement Clock

My pal (let’s call him by the name “The Big C”) tasted the forbidden fruit several years ago when he left his corporate law job in New York City and moved to sunny Lisbon with his wife and their adorable baby. It didn’t work out. The Big C switched to a local law firm (unfortunately, with a decidedly local paycheck). He was only earning a fraction of his NYC biglaw salary and so a couple of years ago, he and his wife opted to move back to the City. His previous firm was anxious to take him back and even made him a partner.

But the hours are intense and working in the biglaw NYC milieu is both tiring and stressful (as I know first-hand). The Big C is looking forward to becoming financially independent - at which point all options are on the table (including an early retirement). He and I were chatting the other day and the Big C told me that he was “counting down the days.”

My ears perked up. “Oh?” I said. “How, specifically?”

The Big C laughed and replied he wasn’t literally counting the days… “but I sure wish I could.”

Good news, Mr. C! Here is a free spreadsheet to enable you (and any of my readers) to do PRECISELY that.

It’s simple to use.

(1) Input the amount you plan to save each year.

(2) Input your desired retirement number.

(3) Input your current portfolio - just the ticker symbols and number of shares.

That’s it! The spreadsheet does all the rest. It will automatically fetch current stock prices, current dividends, average annual returns for the past year, and then crunch all those variables to project the exact date when the Big C might hit his magical retirement number. Take a look!

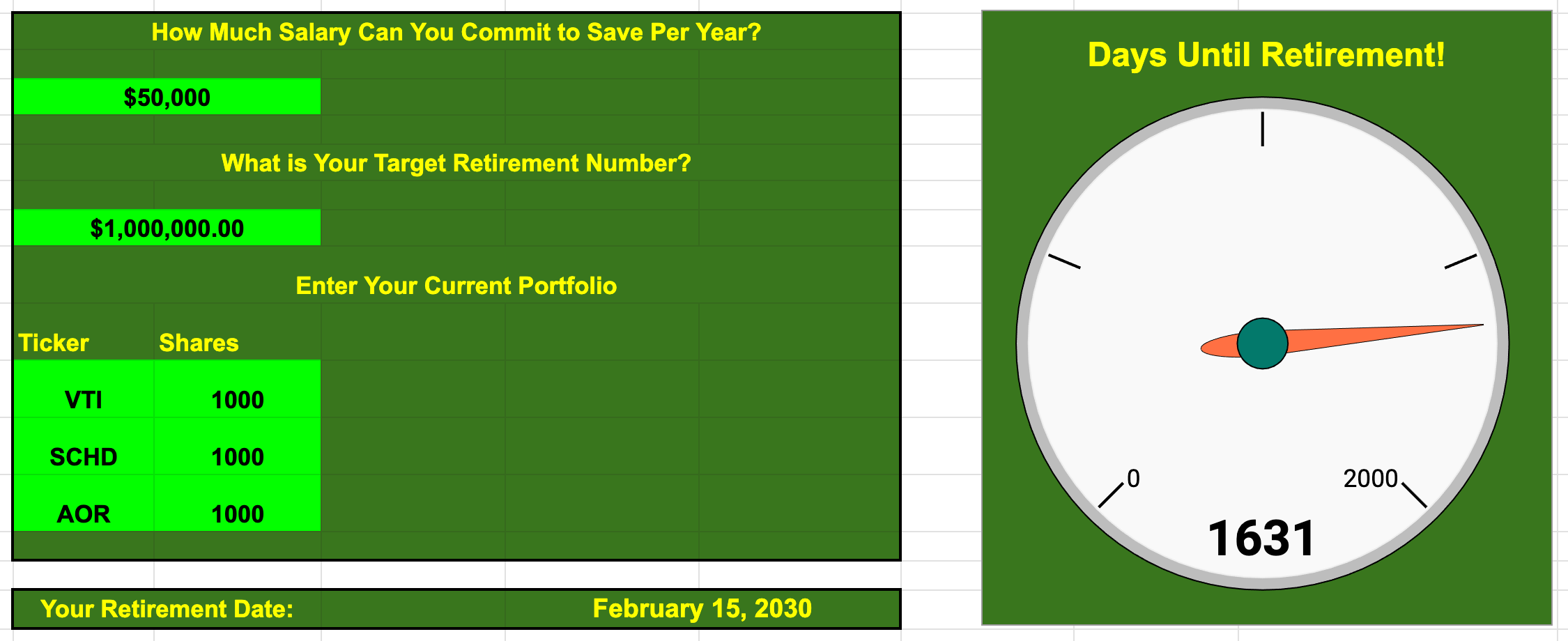

Here we can see that the Big C plans to save $50k per year, and owns a 1,000 shares apiece of three funds - a total market stock fund (VTI), a dividend growth fund (SCHD) and balanced stock and bond fund (AOR). Assuming that he plows all dividends back into his portfolio and invests $50k per year across these three funds in the same proportions that he owns today, the Big C should hit his $1,000,000 target on February 15th, 2030. Roughly 1631 days from today.

Now, as market prices shift and dividend payments change, so too will the Big C’s projected retirement date. The future is in a constant state of flux, but as time goes by and the Big C adds more and more shares to his portfolio, the number of days until retirement should start to drop lower and lower.

Let’s see how.

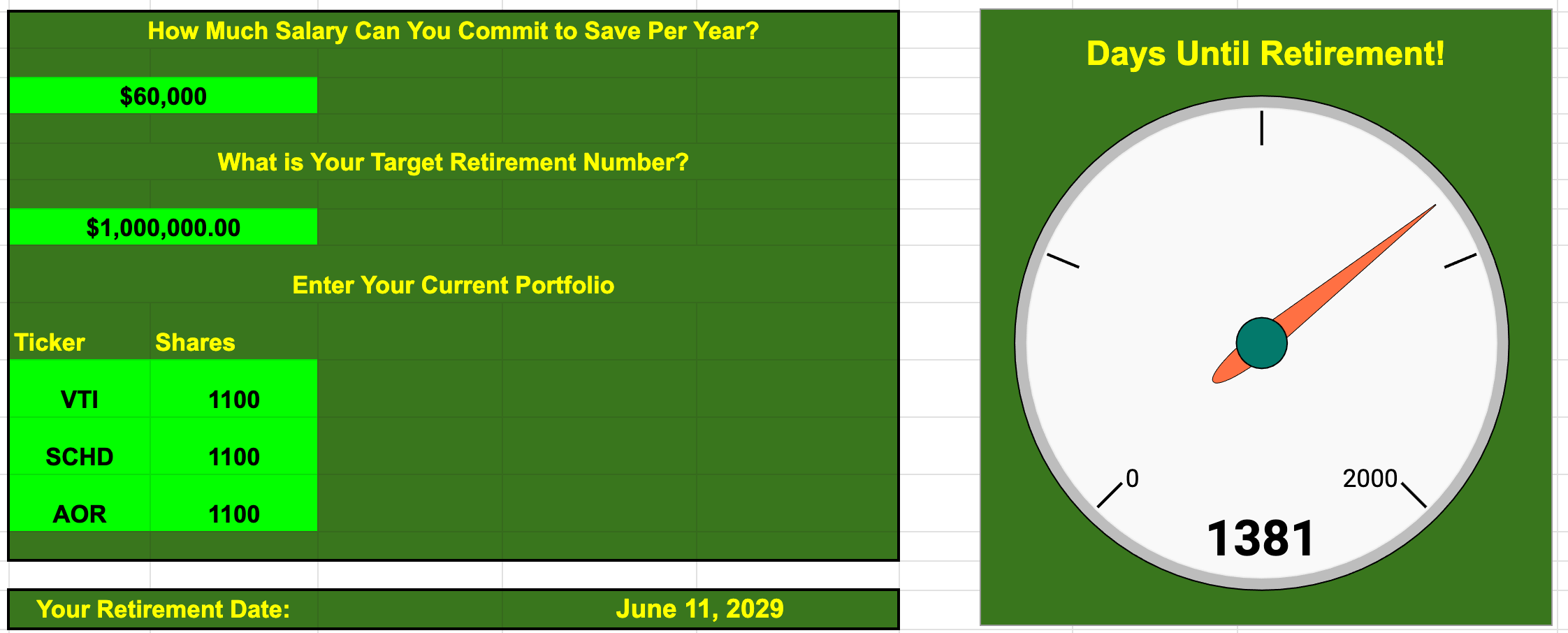

Imagine The Big C decides to buy another 100 shares of each of his 3 portfolio funds. Not only that, but he also decides to up his retirement savings each year from $50,000 to $60,000.

Whoa. Those minor adjustments have a huge impact on his projected retirement date, saving him 250 days.

Conclusion:

Time is money. Here is a tool to help translate that fact into something easy to visualize. In fact, The Big C now finds it somewhat more compelling to make those bi-weekly contributions to his portfolio. Saving money can start to feel pretty abstract. But saving TIME???? You know exactly what you’re buying. Bad day at work? Go buy some extra shares for your portfolio and tick off how many FEWER days like that you’re facing.

Can you modify this spreadsheet for your own purposes? Of course. You can add rows and ticker symbols and adjust the calculations accordingly. Like any financial tool, this one isn’t investment advice and offers no sort of guarantee as far as future returns go. Nor can I guarantee that the data feeds used to power this spreadsheet are accurate. that said, if you are interested in going from “counting down the days” to “scientifically counting down the days,” then feel free to download a copy for yourself and adapt it to your own personal uses and needs.

Postscript: Find the Easter Egg!!!! What happens to your chart if your projected retirement date equals today (or earlier)?

Ever since I started reading Reddit early retirement boards, I learned the answer to a question that has burned bright and unanswered in my consciousness for years: is there a secret code or handshake for those who hit their retirement goals? Based on hundreds of early retirement Reddit posts, the answer is resounding “yes.” I have now built that code into this spreadsheet and will leave it to the reader to uncover the secret!

(Hint: the acronym does NOT stand for “good for you!”)